Business Review

Tools

-

Email Alert Request

-

Share this Page

-

Bookmark

-

Print this Page

In 2025, the national total electricity consumption increased by 5.0% year-on-year to 10.37 trillion kWh, marking the first time that annual national total electricity consumption has exceeded 10 trillion kWh. Electricity demand was effectively supported by China’s ongoing pro-growth policies and significant progress in emerging industries. Under the “Dual Carbon Goals”, new energy will continue to replace fossil fuels in an orderly manner. In 2025, newly added electricity generation from new energy accounted for 97.1% of the increase in national electricity consumption, demonstrating continuous growth in green power supply capacity and the accelerating pace of China’s green and low-carbon transition.

Both wind power and photovoltaic power operations of Group continued to maintain revenue growth, primarily attributable to the consolidation of several wind power and photovoltaic power project companies into the Group pursuant to the external acquisitions by Wu Ling Power under the Asset Pre-Restructuring (please refer to the section titled “Material Acquisitions and Disposals” below for details), as well as the acquisitions and commencement of operations of various new power generating units during the year. However, the implementation of the fully market-based renewable energy on-grid tariff policy by the national government resulted in adjustments to average on-grid tariffs, leading to a year-on-year decline in profit from these segments.

The Group’s thermal power segment was benefited from reduction in fuel costs and implementation of effective coal procurement measures, which contributed to a positive profit growth during the year. However, the reclassification of a coal-fired power generation company with a total installed capacity of 1,260MW from a subsidiary to an associate of the Company at the end of last year (please refer to the Company’s announcement dated 31 December 2024 for details), resulted in a year-on-year decline in electricity sales and revenue.

Hydropower performance was adversely affected by reduced rainfall in the regions where the Group’s hydropower plants operate, resulting in lower electricity generation and a corresponding decline in both revenue and profit from the hydropower segment. Profit in hydropower segment was further affected by a one-off tax expense of approximately RMB357 million arising from the group reorganization under the Asset Pre-Restructuring.

Completion of the Asset Restructuring took place on 31 October 2025 (please also refer to the section titled “Material Acquisitions and Disposals” below for details). Upon completion, the Company, together with its wholly-owned subsidiary, Guangxi Company, held approximately 55.13% equity interest in SPIC Hydropower, which was formerly known as Yuanda Environmental at the time the Asset Restructuring was entered into. Accordingly, SPIC Hydropower has become a subsidiary of the Company and its financial results have been consolidated into the Group’s consolidated financial statements. The acquisition has strengthened the Group’s presence in the capital markets in both Hong Kong and the PRC.

Following the completion of the Asset Pre-Restructuring and Asset Restructuring, the Group recognized gains on bargain purchase of approximately RMB322 million, which partially offset the one-off tax expense of approximately RMB357 million arising from the group reorganization transactions under the Asset Pre-Restructuring.

For the year ended 31 December 2025, the profit attributable to equity holders of the Group amounted to RMB3,404,070,000 (2024: RMB3,861,822,000). Profit attributable to ordinary shareholders of the Company amounted to RMB2,910,226,000 (2024: RMB3,364,381,000). Basic earnings per share was approximately RMB0.24 (2024: RMB0.27). As at 31 December 2025, net assets per share (excluding non-controlling interests and other equity instruments) was approximately RMB3.47.

During the year under review, the development and performance of the Group’s principal businesses were as follows:

As at 31 December 2025, the consolidated installed capacity of the Group’s power plants was 54,753.7MW, representing a year-on-year increase of 5,362.8MW or 10.86%. The Group’s consolidated installed capacity of clean energy (inclusive of hydropower, wind power, photovoltaic power, natural gas power and environmental power) was 44,933.7MW, accounting for approximately 82.07% of the total consolidated installed capacity of the Group, and representing an increase of approximately 1.95 percentage points as compared to the previous year.

The details of consolidated installed capacity of the Group as at 31 December 2025 are set out as follows:

The Group’s power generating units that commenced commercial operation and those that were acquired during the year are presented by type as follows:

The year 2025 is a critical year that sets the stage for transitioning to and planning of the national “15th Five-Year” plan. The Company will actively support the national initiative by focusing on the development of green and low-carbon energy, accelerating the construction of novel power systems, and staying committed to high-quality development. The status of key projects during the year under review are as follows:

Integrated Wind-Photovoltaic-Thermal-and-Storage Demonstration Project of CP Pu’an

The Integrated Wind-Photovoltaic-Thermal-and-Storage Demonstration Project of China Power (Pu’an) New Energy Co., Ltd.* (中電(普安)新能源有限責任公司), a subsidiary of the Company, has a planned installed capacity of 1,000MW, including 700MW of photovoltaic power generation, 300MW of wind power generation and energy storage facilities at different stages. Located in Guizhou Province, the PRC, the project adopts centralized-controlled intelligent dispatching to realize 24-hour monitoring of equipment operation across all power plants. With in-depth integration of advanced models such as the development concept of smart power stations, the project ensures excellent, safe and efficient operation. It is not only one of the key projects in Guizhou Province’s “14th Five-Year” plan for power development, but also a representative example of energy structure innovation and excellence in regions covered by the Southern Power Grid. In 2025, Xicaochong and Jinzhuping photovoltaic power stations under the project, with a total capacity of 166MW, were connected to the power grid for power generation and commenced commercial operation. The project can not only effectively reduce the emission of air pollutants to improve environmental quality, but also promote diversification and transformation of local industries to help addressing challenges related to local employment.

Integrated Source-Grid-Load-and-Storage Project of Xinjiang Power

The 300MW Integrated Source-Grid-Load-and-Storage Project of China Power Hutubi New Energy Co., Ltd.* (中電呼圖壁新能源有限公司), a subsidiary of the Company, was connected to the power grid at full capacity in 2025. Located in Hutubi County, Xinjiang Uygur Autonomous Region, the PRC, the project was constructed by making full use of the abundant sunlight resources in the locality and is equipped with energy storage equipment of 75MW/300MWh, strictly aligning with the national policy requirements for “synergistic development of Source-Grid-Load-and-Storage” within the innovative power system. Upon putting into operation, the project is expected to save substantial standard coal consumption and reduce carbon dioxide emission on an annual basis, hence help mitigating environmental pollution, protecting the ecological environment and promoting local economic development.

Dajia Pingge Hydropower-Photovoltaic Complementary Agricultural Photovoltaic Power Generation Project

The 200MW Hydropower-Photovoltaic Complementary Agricultural Photovoltaic Power Generation Project of Liping Qingshuijiang New Energy Co., Ltd.* (黎平清水江新能源有限公司), a subsidiary of the Company, has commenced commercial operation at full capacity in 2025. Located in Liping County, Guizhou Province, the PRC, the project fully utilizes renewable energy without occupying basic farmland and woodland. With no exhaust gas, wastewater and solid waste generated throughout the process of power generation, the project can effectively protect the local ecological environment. Concurrently, it promotes the integrated development of the photovoltaic power generation industry and agriculture, supporting the diversification and upgrade of local industries. This aligns intensively with the national rural revitalization strategies and policies for green energy development, thereby enhancing ecological and social benefits at the same time.

Liumaohu Wind Power Project

The 200MW wind power project of Mishan Beiling Wind Power Generation Co., Ltd.* (密山市北嶺風力發電有限公司), a subsidiary of the Company, was connected to the power grid and commenced operation at full capacity in 2025. Located in Heilongjiang Province, the PRC, the project is equipped with 40 wind turbines, including the construction of energy storage and peak-load shaving systems as ancillary facilities. Upon putting into operation, the project is expected to save substantial standard coal consumption and reduce carbon dioxide emission on an annual basis, providing major support for the development of integrated energy systems in Mishan City and Heilongjiang Province.

Binzhou Fishery-Photovoltaic Complementary Photovoltaic Power Generation Project

The 200MW Fishery-Photovoltaic Complementary Photovoltaic Power Generation Project of Binzhou Power Investment New Energy Development Co., Ltd.* (濱州電投新能源發展有限公司), a subsidiary of the Company, has been put into operation in 2025. Located in Shandong Province, the PRC, the project adopts a “photovoltaic power generation + aquaculture” development model. It makes full use of the salt-alkali tidal flat land resources to achieve efficient composite land use and promote in-depth integration of photovoltaic power generation and the fishery industry. Upon putting into operation, the project not only effectively facilitates the green and low-carbon transformation and creates vast job opportunities in the locality, playing an active role in promoting steady growth and structural adjustment and improving people’s livelihood in the local region.

Photovoltaic Power Generation Project of Yuci District, Jinzhong City

The Yuci 300MW (100MW in Phase I) photovoltaic power generation project of Jinzhongshi Yuciqu Zhongling New Energy Co., Ltd.* (晉中市榆次區眾凌新能源有限公司), a subsidiary of the Company, has been put into full operation in 2025. Located in mountainous and hilly terrain at elevations ranging from 768 to 1,814 meters, the project fully utilizes idle land resources. With a DC-side installed capacity of 120MW peak, it comprises 54 planned photovoltaic sub-arrays with a total of 252 300-kW string inverters and 126 196-kW string inverters installed. The average annual power generation is projected to be approximately 165,495MWh. Development of this project contributes to the upgrade of the local industrial structure and promotes the growth of the local new energy industry, yielding sound social benefits and economic returns.

Datonghu Fishery-Photovoltaic Complementary Photovoltaic Power Generation Project

The two Fishery-Photovoltaic Complementary Photovoltaic Power Generation Projects with installed capacity of 290MW in aggregate of China Power (Datonghu) Energy Development Co., Ltd.* (中電(大通湖)能源發展有限公司), a subsidiary of the Company, was connected to the power grid at full capacity and commenced power generation in 2025. Located in Hunan Province, the projects include the construction of a 220kV booster station and a 220kV transmission line as ancillary facilities. The photovoltaic power station is designed based on the principle of “unmanned shift and minimal staff on duty”. It adopts a fishery-photovoltaic complementary model of “power generation on the solar panels while fish farming below” to realize efficient and compound use of land resources. The project can save standard coal consumption, reduce emissions of carbon dioxide, sulfur dioxide and nitrogen oxides, and promote the clean use of energy in rural areas, thereby bringing significant economic, environmental and social benefits for the fishery industry, the power industry and environmental protection.

Persisting in prioritizing technological innovation, the Group continued to press ahead with its digital and intelligent transformation alongside development of the presence in strategic emerging industries, and stepped up its investment in technological research and development. By focusing on key technological innovations and the application of digital and intelligent technologies within the clean energy sector, it aimed to further consolidate its competitive edge in the sector. In addition, we have actively nurtured and introduced high-end technological talents, accelerated the incubation of energy-related strategic emerging industries, thereby promoting the conversion of technological innovation achievements into effective productivity, thus empowering high-quality development of the industry.

Intelligent Energy Storage

In 2025, Xinyuan Smart Storage, a subsidiary of the Company, achieved major breakthroughs in aspects such as research and development of energy storage systems, market expansion and operational capabilities.

During the year, Xinyuan Smart Storage completed various tasks relating to construction of laboratories to high standards, strictly adhering to the standard specifications for the construction of national-class laboratories. This included completion of 7 large-scale energy storage test platforms, the filing of application for 56 invention patents, the formulation of 20 standards, and the reporting of 12 exemplary achievements to the Ministry of Emergency Management. In addition, a key laboratory successfully passed the on-site inspection and acceptance assessment conducted by the Ministry of Emergency Management of the PRC.

Breakthrough progress was made in overseas market deployment, securing order contracts relating to intelligent management for two 100-MW-class energy storage projects in Chile and Kazakhstan. The first overseas cloud platform hub for energy storage was built in Riyadh, Saudi Arabia. Equipping with regional data compliance service capabilities abroad, it marks the official launch of Xinyuan Smart Storage’s intelligent energy storage services in the international market.

Green Power Transportation

In 2025, Qiyuanxin Power, an associate of the Company, continued to put greater focused efforts in the charging and battery-swap sector. It fostered significant results in both domestic and international market expansion and business development, further consolidating its leading position within the industry. With major breakthroughs in overseas operations, Qiyuanxin Power has successfully partnered with a global mining giant to deliver the first batch of mining trucks and battery swap stations to a mining site in Mongolia. Within the first month of operation, more than 500 battery swaps were completed, totaling more than 250,000kWh of swapped power. This represents a great move in the global expansion of transportation and energy integration business of Qiyuanxin Power, effectively promoting its overseas market development.

As for the domestic market, Qiyuanxin Power’s charging and battery-swap network continued to expand in both construction and operational scale. As at the end of 2025, more than 1,600 charging and battery-swap stations for heavy-duty trucks were either under or completed construction, covering 208 prefecture-level cities nationwide. With the cumulative operational mileage of electric vehicles (EVs) served exceeding 4.4 billion kilometers, Qiyuanxin Power has maintained the industry’s top market share in battery-swap stations for heavy-duty trucks. The construction of charging and battery-swap corridor yielded substantial results. Not only have key trunk routes such as National Highway G110, the Ningbo-Jinhua Expressway, and the Hainan Ring Expressway been connected to the corridor, but the core objectives of China’s Transportation Power Initiative for developing into a strong transportation nation have also been successfully accomplished: establishing and operating China’s longest charging and battery-swap corridor for heavy-duty trucks spanning 7 provinces/regions and 13 cities, with a total length exceeding 2,200 kilometers, enabling cross-regional coordinated operations. Meanwhile, significant achievements were made in technological innovation and power grid interaction. Qiyuanxin Power successfully fulfilled the demonstration and verification of aggregation and interaction with power grids of 100MW-class battery swap stations, showcasing excellent grid-connected operational characteristics and providing robust support for steady grid operation.

In terms of the development of standards, Qiyuanxin Power continued to play its role as a leader of the industry. It spearheaded and participated in formulating dozens of various international, national, and industry standards in aggregate. The ongoing improvement of its system of standards has further consolidated Qiyuanxin Power’s influence in terms of technologies and standards within the industry.

Projects Under Construction

As at 31 December, 2025, the aggregate installed capacity of projects under construction was 4,467MW, all of which were clean energy projects. These included various large-scale wind power and photovoltaic power generation projects located in Shanxi Province, Shandong Province, Hebei Province, Guizhou Province, and Jiangsu Province.

New Development Projects

The Group is currently conducting preliminary work on new projects (including those submitted to the Chinese government for approval) with a total installed capacity of approximately 28,000MW. All of them are clean energy projects, primarily located in regions with development potential such as Shandong Province, Shanxi Province, Xinjiang Uygur Autonomous Region, and Heilongjiang Province. These projects include the Shandong Peninsula South offshore wind power project with a total installed capacity of 9,000MW, the Xinjiang Hemi Balikun 1,000MW wind power project, the SPIC 500MW wind power project under the 170th Regiment of Baiyang City, Ninth Division, and the Yuci 500MW photovoltaic power generation project of Jinzhong City, Shanxi Province.

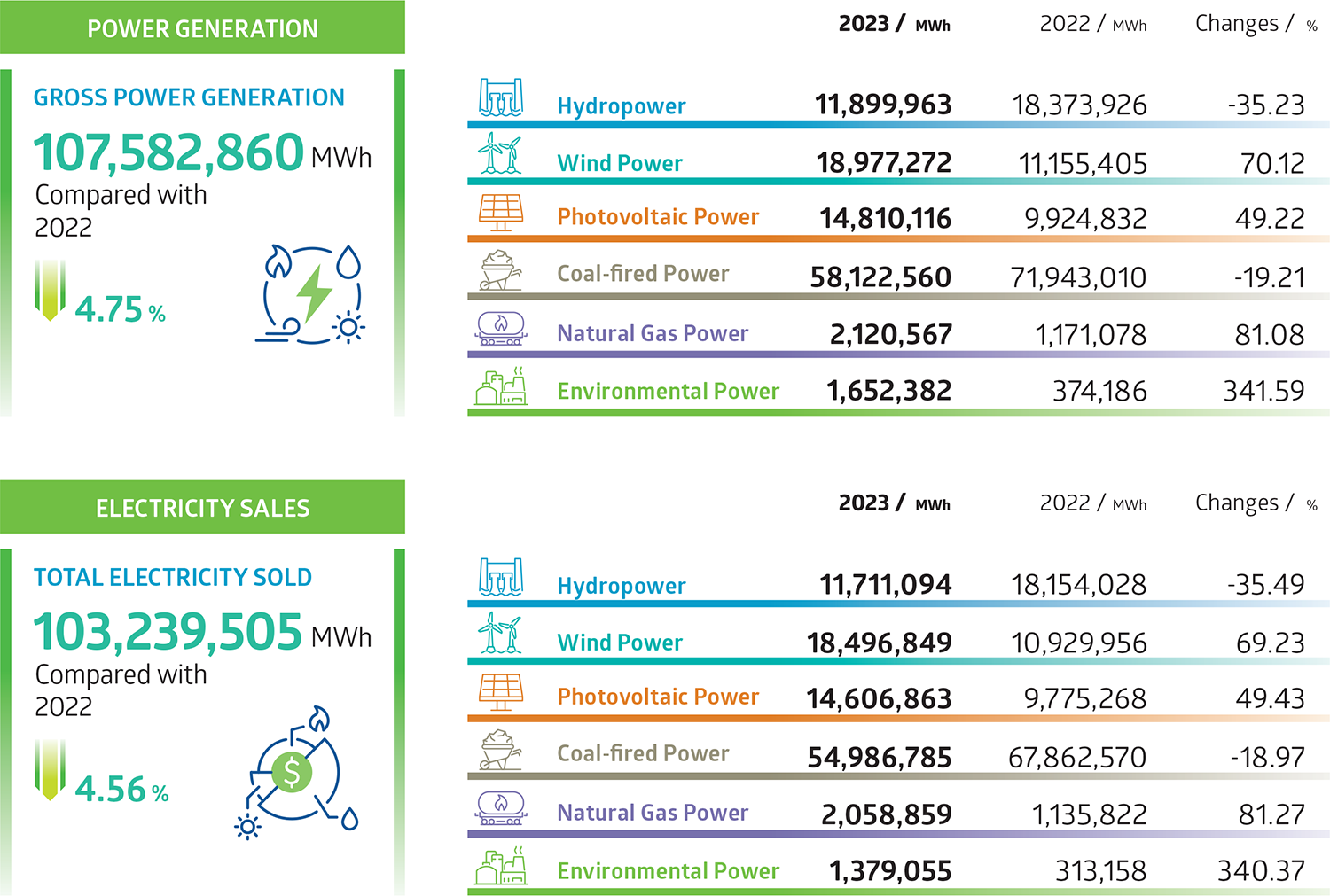

In 2025, the details of power generation and electricity sold by the Group are set out as follows:

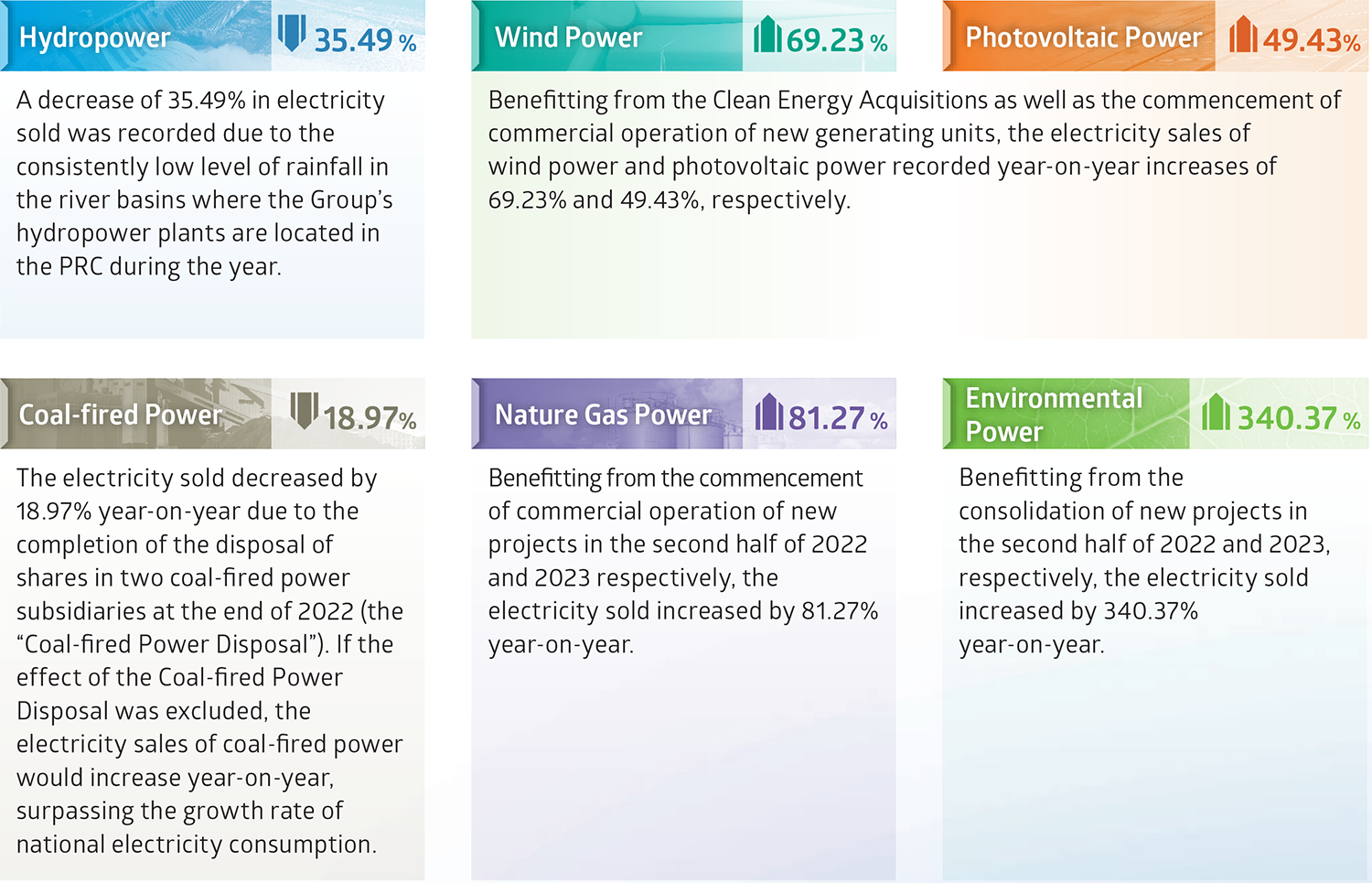

In 2025, the total electricity sold by the Group amounted to 126,332,861MWh, representing a decrease of 1.27% as compared with the previous year. The changes in electricity sold by each power segment as compared with the previous year are as follows:

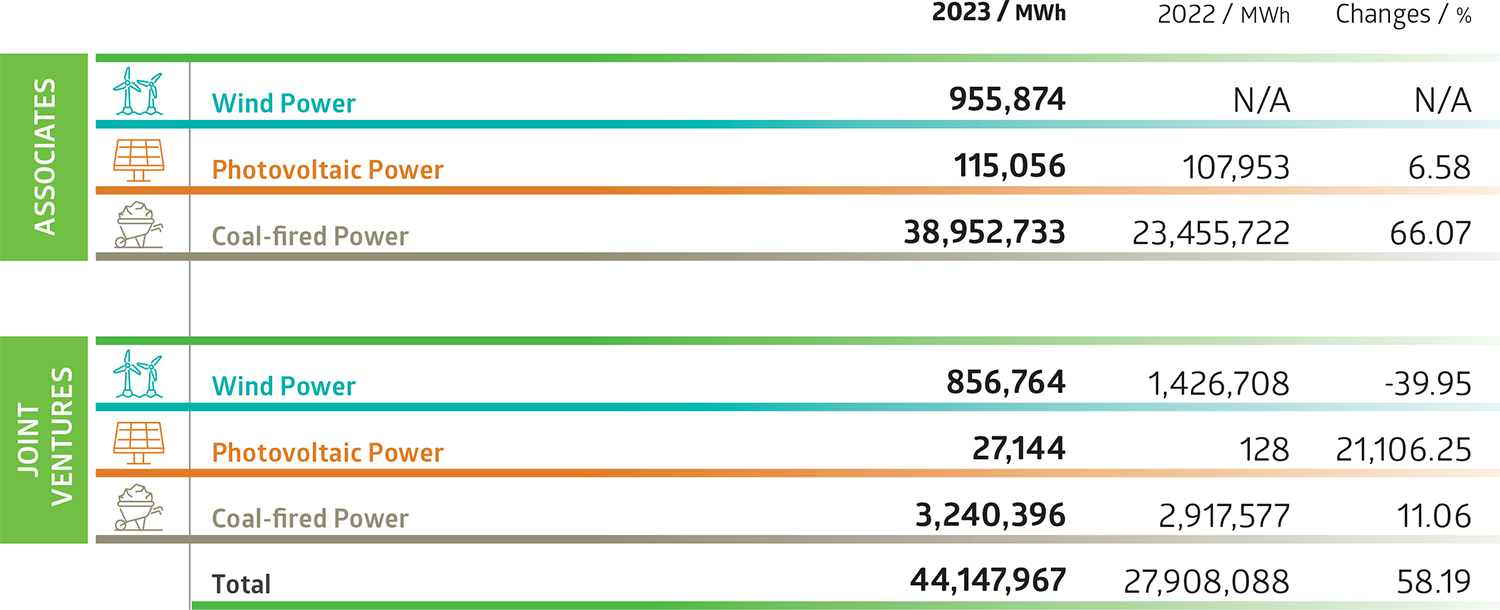

In 2025, the details of electricity sold by the Group’s main associates and joint ventures are set out as follows:

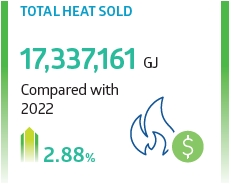

In 2025, the total heat sold by the Group’s subsidiaries reached 24,905,715GJ, representing an increase of 2,035,200GJ or 8.90%, as compared to the previous year. This growth was primarily benefited from the Group’s proactive market expansion initiatives, which significantly expanded its customer base, as well as an increase in heat demand. Conversely, the Group’s main associates and joint ventures recorded total heat sold of 18,138,731GJ, a decrease of 319,081GJ, or 1.73%, year-on-year, largely due to the reduction in heating supply of an associate. The profit related to the heat sales operation of the Group were classified as other gains and losses in the consolidated statement of profit or loss. During the year, profits generated from sales of heat, trading of coal, coal by- products, spare parts and others totaled RMB343,590,000 (2024: RMB285,740,000), representing an increase of 20.25% as compared to the previous year.

To further strengthen its core capabilities in heat supply operations and enhance the overall heat supply reliability, the Group commenced and completed a number of renovation projects in 2025. They principally included the Fuxi Power Plant Siliya Heat Supply Renovation Project, the Sanjiang New Area Sichuan Times Heat Supply Renovation Project, the Shentou Power Central Heat Supply Project, the Shangqiu Thermal Power Heat Supply Network First Station Renovation Project, the Bazhou Environmental Oilfield Farm Heat Supply Engineering Project, the Aileda Tuowei Branch Pipeline Network Construction Project of China Power (Chengdu) Comprehensive Energy Co., Ltd. and other projects, all of which will contribute to the continuous improvement of its heat supply capacity.

The Group has actively engaged in the market-oriented reform of the national power industry, strengthened its research on power market policies and regulations, particularly in core aspects such as trading of spot electricity, green certificate/green power and carbon emission allowances, and continuously optimized its market trading strategies. The Group has maximized its market power sales and expanded its market share through increased participation in market-power transactions. Subsidiaries in various provinces have also established their power sales centers to attract and retain target customers. During the year, the trading volume of green certificate and green power increased by approximately 57% and 17% respectively compared to the previous year.

In 2024, the new tariff for coal-fired power was implemented nationwide to optimize coal-fired power revenues through a dual structure of “capacity tariff” plus “volume tariff”. While the premium margin in market-traded power tariffs experienced a slight decline, primarily due to increased participation of other power sources in the spot market, which drove down market-traded power tariffs, the capacity tariff (i.e. determined by way of the calculation on recovering a certain percentage of the fixed costs of the coal-fired power generating units) provided a stable comprehensive tariff.

Despite a low premium percentage relative to the benchmark tariff, the comprehensive tariff after taking into account the capacity-tariff basically remained stable, which demonstrated the adjusting impact of the capacity-tariff policy on market-trading-tariff.

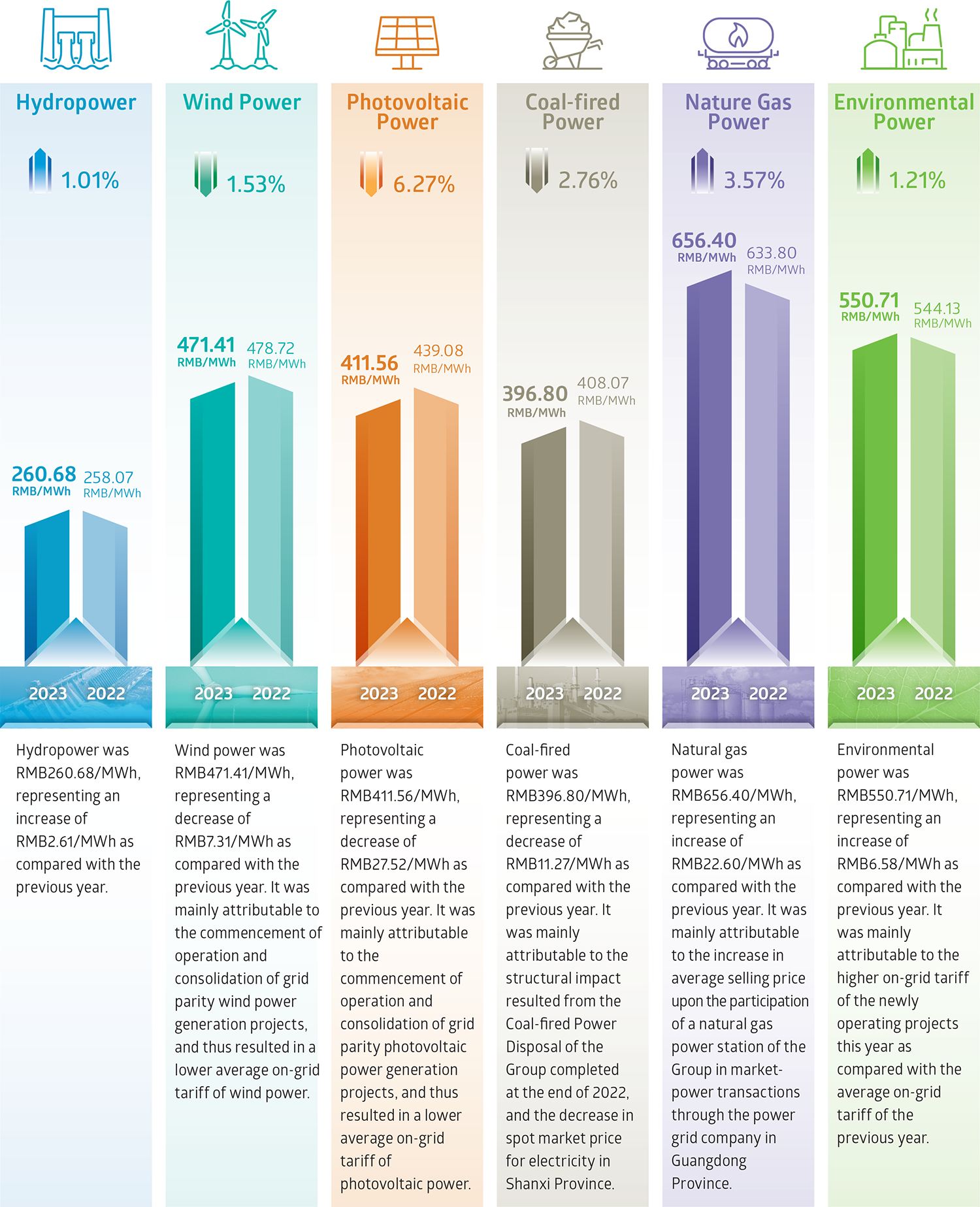

Starting 1 June 2025, all electricity generated by China’s renewable energy power sources, namely photovoltaic power as well as onshore and offshore wind power, shall fully participate in the spot power market and be traded at market prices. In this context, the average on-grid tariffs of electricity generated by the Group across each power segment in 2025, compared with the previous year, were as follows:

Due to intensifying competition in the energy storage industry compared with the previous year, the average unit price of products experienced a year-on-year decline. This aggressive competitive landscape pressured profit margins and resulted in a year-on-year reduction in both revenue and profit. As a result, revenue from the energy storage business amounted to RMB2,304,314,000, representing a year-on-year decrease of RMB1,603,928,000 or 41.04%. Profit for the year was RMB11,886,000, which represents a negative variance of RMB74,694,000 as compared to the previous year.

| Address | Suite 6301, 63/F, Central Plaza, 18 Harbour Road, Wanchai, Hong Kong |

| Phone | (852) 2802-3861 |

| Fax | (852) 2802-3922 |

| ir@chinapower.hk |