Operating Results

Tools

-

Email Alert Request

-

Share this Page

-

Bookmark

-

Print this Page

In 2025, the net profit of the Group amounted to RMB5,918,162,000, representing a decrease of RMB621,728,000 or 9.51% as compared with the previous year.

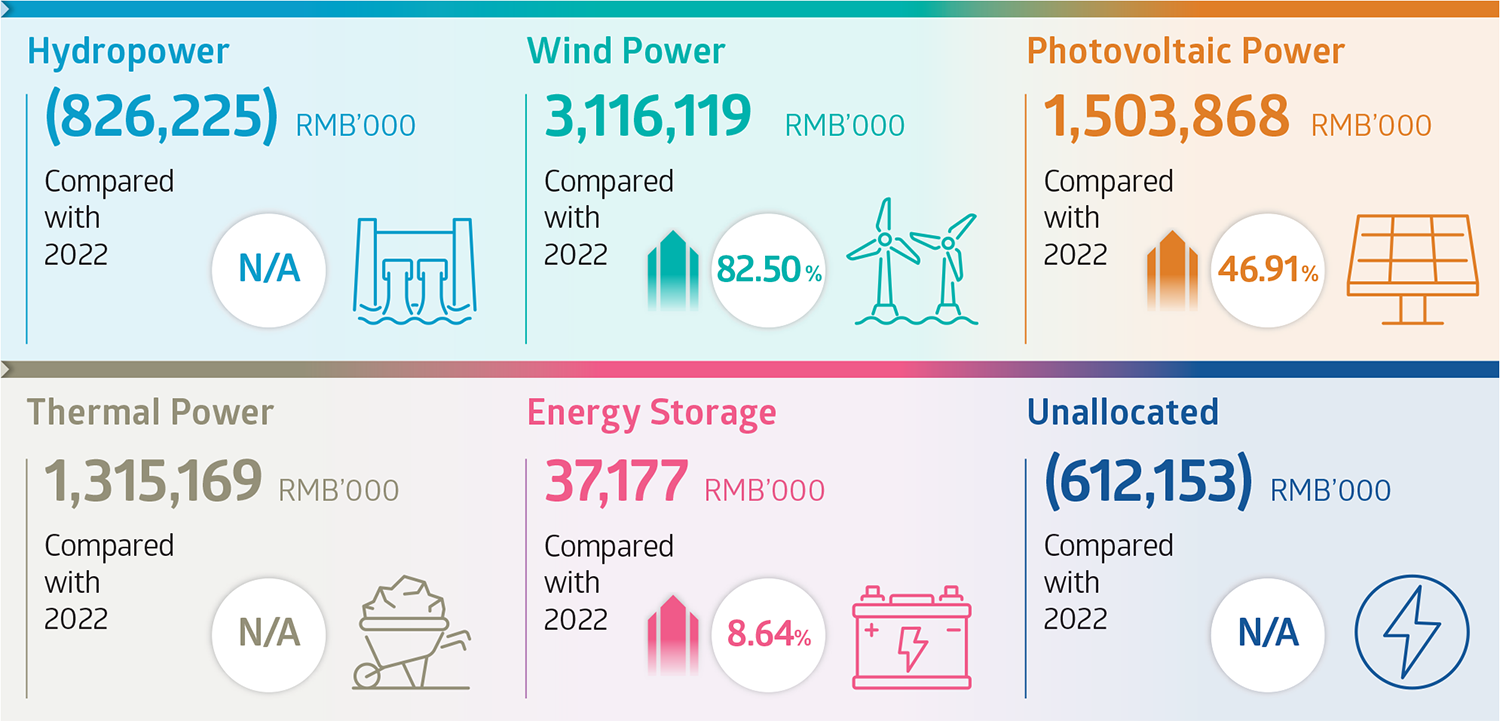

In 2025, the net profit (loss) of each operating segment and their respective changes over the previous year were as follows:

As compared with 2024, the changes in net profit were mainly due to the following factors:

The revenue of the Group was primarily derived from the sales of electricity and energy storage-related services. In 2025, the Group recorded a revenue of RMB49,029,459,000, representing a decrease of 9.56% as compared to RMB54,212,792,000 of the previous year.

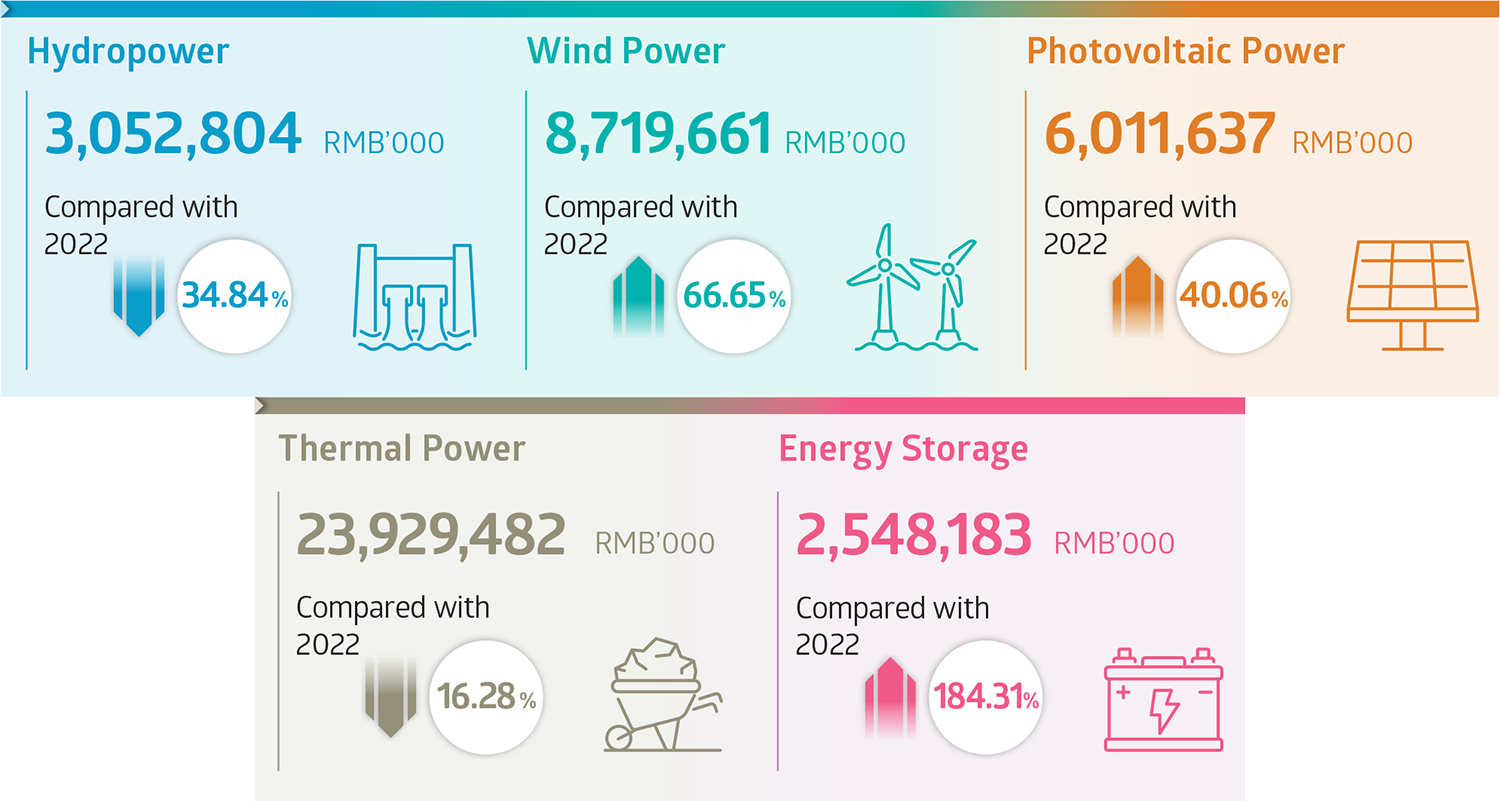

In 2025, the details of revenue of each operating segment are set out as follows:

Revenue from hydropower decreased by RMB31,765,000, which was mainly attributable to the decrease in power generation as a result of lower average rainfall in the river basins where the Group’s hydropower plants are located during the year.

Revenue from wind power and photovoltaic power increased by RMB1,221,911,000 in total, primarily due to the consolidation of several project companies as part of the Asset Pre-Restructuring, as well as the acquisitions and commencement of operations of various new power generating units during the year.

Revenue from thermal power decreased by RMB4,769,551,000 year-on-year, primarily due to the reclassification of Pingwei Power from a subsidiary to an associate of the Company at the end of last year.

Revenue from energy storage decreased by RMB1,603,928,000 year-on-year. The intensified competitive landscape pressured both business volume and average unit prices of energy storage products, leading to a decline in revenue.

Operating costs of the Group mainly consist of fuel costs, repairs and maintenance expenses for power generating units and facilities, depreciation and amortization, staff costs, subcontracting costs, cost of sales of energy storage equipment, consumables, and other operating expenses. In 2025, the operating costs of the Group amounted to RMB42,576,792,000, representing a decrease of 6.05% as compared to RMB45,319,966,000 in the previous year. The decrease was primarily driven by a year-on-year decrease in both fuel costs and cost of sales of energy storage equipment. This downward trend was partially counteracted by the inclusion of SPIC Hydropower, and various project companies into the Group’s consolidated financial statements following the completion of the Asset Restructuring and Asset Pre-Restructuring. Additionally, the commencement of operations of new power generating units resulted in additional costs that partially absorbed the cost savings.

Total Fuel Costs

The total fuel costs decreased by RMB4,372,819,000 or 26.73%. The decline was mainly attributed to the deconsolidation of Pingwei Power (engaged in coal-fired power generation business) following its reclassification from a subsidiary to an associate of the Company at the end of last year. This structural change in assets holding, coupled with a year-on-year decrease in unit fuel cost of the Group’s coal-fired power operations, resulted in an improved cost profile for the year.

Unit Fuel Cost

The average unit fuel cost of the Group’s coal-fired power business was RMB232.76/MWh, representing a decrease of 13.98% as compared to RMB270.58/MWh in the previous year. In the first half of 2025, domestic thermal coal market experienced a continuous increase in supply coupled with weak demand growth, causing prices to drop to multi-year lows. During the second half of the year, as government authorities moved forward with production capacity audits (enforcing limits on over-production), market supply tightened. This regulatory pressure caused coal prices to stabilize and rebound; however, the market weakened again toward the end of the year. To capitalize on opportunities arising from these price fluctuations, the Group actively optimized its cost management strategies, leveraging low-cost windows to secure favorable procurement terms and drive down overall fuel expenditures. Key initiatives included refining long-term contract structures, enhancing logistics efficiency, and deepening specialized coal-blending management to unlock the full economic benefits of co-firing.

Depreciation and Staff Costs

Depreciation of property, plant and equipment and the right-of-use assets and staff costs increased by RMB2,148,263,000 in aggregate, the rise was primarily driven by the consolidation of SPIC Hydropower and various project companies following the recent asset restructuring, as well as the acquisitions and commencement of operations of various new wind power and photovoltaic power generating units during the year.

Cost of Energy Storage Equipment Sales and Subcontracting Costs

The Group’s energy storage segment is principally engaged in sales of energy storage equipment and the provision of subcontracting services for the development and assembly of power stations integrated with energy storage. Of the total subcontracting costs of RMB707,654,000, RMB481,330,000 was attributable to the consolidation of SPIC Hydropower, with the remaining balance attributable to the energy storage segment. The energy storage segment faced a challenging operating landscape as heightened industry competition drove down business volume and average unit prices. In 2025, the cost of energy storage equipment sales and subcontracting costs of the Group totaled RMB1,928,326,000, indicating a decrease of RMB1,284,310,000 or 39.98% as compared to the previous year.

Other Operating Expenses

Other operating expenses increased by RMB216,891,000, or 3.62%, year-on-year, primarily reflecting the expanded scope of consolidation following the recent asset restructuring.

The net gains from other gains and losses increased by RMB822,255,000, or 111.78%, year-on-year. This growth was primarily driven by gains on bargain purchase following the completion of the Asset Pre-Restructuring and the Asset Restructuring, as well as a decrease in impairment of property, plant and equipment.

In 2025, the Group’s operating profit was RMB11,936,366,000, representing a decrease of 1.90% as compared to the operating profit of RMB12,167,191,000 in the previous year.

In 2025, the finance costs of the Group amounted to RMB5,062,776,000 (2024: RMB5,043,066,000), representing an increase of RMB19,710,000, or 0.39%, as compared to the previous year. This increase was partly as a result of the consolidation of bank borrowings from project companies acquired through the Asset Restructuring and the Asset Pre-Restructuring. The Group has initiated countermeasures by actively advancing debt optimization initiatives, including adjusting the interest rate structure and securing favorable loan conditions, allowing the Group to mitigate the increase in finance costs and offset part of the cost pressure. Looking ahead, the Group will continue to monitor market changes and seize opportunities presented by lower financing interest rates to further optimize its debt structure by replacing high-interest borrowings.

In 2025, the profits from the Group’s share of results of associates was RMB613,764,000, representing an increase of RMB62,619,000, or 11.36%, as compared to the previous year. The reclassification of Pingwei Power from a subsidiary to an associate of the Company at the end of last year, combined with a decrease in average unit fuel costs during the year, contributed positively to the growth in the Group’s share of results of associates.

In 2025, the profits from the Group’s share of results of joint ventures was RMB219,742,000, representing an increase of RMB38,287,000, or 21.10%, as compared to the previous year. This increase was largely attributable to the strong performance of coal-fired power generation business.

In 2025, the income tax expense of the Group was RMB1,940,587,000, representing an increase of RMB469,797,000, or 31.94%, as compared to the previous year. The increase in income tax was primarily attributable to income tax expense incurred in connection with the group reorganization under the Asset Pre-Restructuring.

At the Board meeting held on 20 March 2026, the Board recommended the payment of a final dividend for the year ended 31 December 2025 of RMB0.168 (equivalent to HK$0.1911 at the exchange rate announced by the People’s Bank of China on 20 March 2026) per ordinary share (2024: RMB0.162 per ordinary share), totaling RMB2,078,185,000 (equivalent to HK$2,363,936,000) (2024: RMB2,003,964,000), which is based on 12,370,150,983 shares in issue on 20 March 2026.

The dividend payout ratio for 2025, calculated as dividend per share, divided by earnings per share, was 70% (2024: 60%). The Board confirmed that the dividend decisions made in 2025 were in accordance with the Company’s dividend policy, which mandates a minimum payout ratio of no less than 50%. The increase in the dividend payout ratio for 2025, as compared to the previous year, underscores the Board’s commitment to delivering enhanced returns to shareholders.

For comparability purposes, the 2024 dividend of RMB0.162 per ordinary share and the 2024 dividend payout ratio of 60% referred to above are presented excluding the one-off special dividend of RMB0.05 per ordinary share declared to mark the 20th anniversary of the Company’s listing on the Hong Kong Stock Exchange in 2024.

As at 31 December 2025, the carrying amount of equity instruments at FVTOCI was RMB9,272,721,000, accounting for 2.52% of total assets, including listed equity securities of RMB7,273,109,000 and unlisted equity investments of RMB1,999,612,000.

Listed equity securities represent the equity interests in Shanghai Power held by the Group. As at 31 December 2025, the Group held 12.88% (31 December 2024: 12.90%) of the issued share capital of Shanghai Power, the A shares of which are listed on the SSE. These securities were categorized as level 1 financial assets of fair value measurements, and their fair values increased by 118.32% as compared with RMB3,331,389,000 as at 31 December 2024.

Unlisted equity investments represent the Group’s investment in equity of certain unlisted companies principally engaged in financial services, coal production and electricity trading services respectively. They were categorized as level 3 financial assets of fair value measurements, and their fair values increased by 13.63% from RMB1,759,716,000 as at 31 December 2024.

The valuation methods and key inputs used for measuring the fair values of the above level 3 financial assets were market approach, i.e. fair values of such equity instruments were estimated by calculating the appropriate value ratio based on market multiples derived from a set of comparable listed companies in the same or similar industries. Key inputs were (i) the market value of the said equity interests, (ii) price-to-book ratio (1.05–1.82) and the discount rate for lack of marketability (28.00%) of the comparable companies. The fair value measurement is positively correlated to the above ratios and negatively correlated to the discount for lack of marketability.

The fair value gain on equity instruments at FVTOCI (net of tax) for the year ended 31 December 2025 of RMB2,945,359,000 (2024: gain of RMB195,570,000) was recognized in the consolidated statement of comprehensive income.

On 16 April 2025, the Company, Xiangtou International and Guangxi Company, entered into equity transfer agreements with SPIC Hydropower (formerly known as Yuanda Environmental at the time of the transaction, a company listed on the SSE), pursuant to which (i) the Company and Xiangtou International agreed to transfer 63% and 37% equity interests in Wu Ling Power, respectively, and (ii) Guangxi Company agreed to transfer a 64.93% equity interests in Changzhou Hydropower to SPIC Hydropower, in exchange for new shares to be issued by SPIC Hydropower and cash consideration (the “Asset Restructuring”). For details of the transaction, please refer to the circular of the Company dated 20 May 2025.

On 29 August 2025 and 16 September 2025, following the pre-completion distribution of dividends by Wu Ling Power and Changzhou Hydropower and in compliance with the regulatory requirements of the SSE and the China Securities Regulatory Commission, the Company, Guangxi Company and SPIC Hydropower entered into supplemental agreements to adjust the consideration for the Asset Restructuring and the profit undertaking arrangements contemplated thereunder. For details, please refer to the announcements of the Company on the same dates.

To facilitate the implementation of the Asset Restructuring, Wu Ling Power and Changzhou Hydropower carried out a series of corporate reorganizations (the “Asset Pre-Restructuring”) prior to the Asset Restructuring, which mainly comprised: (1) external acquisitions by Wu Ling Power entered into on 17 January 2025; (2) formation of two new subsidiaries; and (3) intra-group reorganization. For details regarding the Asset Pre-Restructuring, please refer to the announcement of the Company dated 17 January 2025. The external acquisitions by Wu Ling Power were completed on 28 February 2025. Details are set out in note 47 to the consolidated financial information in this annual report.

On 31 October 2025, all conditions precedent to the Asset Restructuring had been satisfied and completion took place. Upon completion, the Company, together with its wholly-owned subsidiary, Guangxi Company, held an aggregate of 2,414,961,831 shares of SPIC Hydropower, representing approximately 55.13% of its share capital. SPIC Hydropower has become a subsidiary of the Company. Please refer to note 47 to the consolidated financial information in this annual report for further details.

On 18 June 2025, the Company, CPI Holding, Guangdong Company and Jieyang Power entered into an equity transfer agreement, pursuant to which the Company agreed to acquire and Guangdong Company agreed to sell 35% equity interest in Jieyang Power at a consideration of RMB36,693,510 plus a post-completion capital contribution of RMB558,600,000, amounting to RMB595,293,510 in total. Jieyang Power, through its wholly-owned subsidiary, holds the development right to two ultra-supercritical coal-fired power generating units with total installed capacity of 2,000MW located in Guangdong Province, the PRC as well as the approval for the development right to an offshore wind power project in the state-controlled waters of Jieyang. The acquisition marks a joint-operation development model of coal-fired power with renewable energy. For details, please refer to the announcement of the Company issued on the same date.

On 17 July 2025, the Company, CPI Holding, Pingmei Shenma (Xinjiang) Energy Co., Ltd.*, Xinjiang Energy and Tuoli Power entered into an equity transfer agreement, pursuant to which the Company agreed to acquire and Xinjiang Energy agreed to sell 31% equity interest in Tuoli Power at a consideration of RMB24,212,147 plus a post-completion capital contribution of RMB285,820,000, amounting to RMB310,032,147 in total. Tuoli Power holds the development right to two ultra-supercritical coal-fired power generating units with a total installed capacity of 1,320MW located in Tuoli County, Tacheng Prefecture, Xinjiang Uygur Autonomous Region, the PRC. The acquisition aims to address the power supply shortfall in the region by leveraging a “coal plus coal-fired power joint operation” industrial model. For details, please refer to the announcement of the Company issued on the same date.

On 12 September 2025, the Company, Shaanxi Yanchang Petroleum Mining Co., Ltd.*, Sichuan Company and Dazhou Energy entered into an equity transfer agreement, pursuant to which, the Company agreed to acquire and Sichuan Company agreed to sell 31% equity interest in Dazhou Energy at a consideration of RMB31,000,000, together with a capital commitment and a post-completion capital contribution of RMB427,800,000 in aggregate, amounting to RMB458,800,000 in total. Dazhou Energy holds the development rights to two ultra-supercritical coal-fired power generating units with a total installed capacity of 2,000MW located in Sichuan Province, the PRC. The project is expected to enhance the overall reliability of the power supply in Sichuan Province and alleviate peak-load pressures on the Sichuan power grid. For details, please refer to the announcement of the Company issued on the same date.

Save as disclosed above, the Group did not have any other material acquisitions and disposals during the year under review.

On 12 February 2026, CCB Investment, the Company and Xinyuan Green Power (a non wholly-owned subsidiary of the Company) entered into a capital reduction agreement, pursuant to which CCB Investment will exit its entire equity interest in Xinyuan Green Power by way of a directed capital reduction of Xinyuan Green Power’s registered capital in an amount of RMB1,665,713,115 for a consideration of RMB2,005,973,156. Immediately after the capital reduction, the registered capital of Xinyuan Green Power shall be reduced from RMB3,665,713,115 to RMB2,000,000,000. The Company’s equity interest in Xinyuan Green Power will be increased from 54.56% to 100% accordingly.

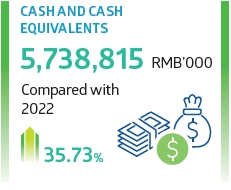

As at 31 December 2025, cash and cash equivalents of the Group were RMB6,378,305,000 (31 December 2024: RMB6,073,616,000). Current assets amounted to RMB57,630,373,000 (31 December 2024: RMB51,638,373,000), current liabilities amounted to RMB92,210,722,000 (31 December 2024: RMB93,182,359,000) and current ratio was 0.62 (31 December 2024: 0.55).

In May 2022, the Company entered into the financial services framework agreement with SPIC Financial for a term of three years, effective from 7 June 2022 to 6 June 2025, pursuant to which SPIC Financial agreed to provide the Group with deposit services, settlement services, loan services and other financial services on a non-exclusive basis. The annual cap in respect of the maximum daily balance of deposit (including accrued interests) placed by the Group with SPIC Financial shall not exceed RMB5.5 billion during the effective term of the framework agreement. As a result of the acquisition of certain clean energy companies, the Company entered into a supplemental agreement to the financial services framework agreement with SPIC Financial in August 2023 to revise the original annual cap in respect of the maximum daily balance of deposit placed by the Group with SPIC Financial from RMB5.5 billion to RMB9 billion, while other principal terms remained unchanged.

In April 2025, the Company entered into a new financial services framework agreement (the “New Financial Services Framework Agreement”) to continue to engage SPIC Financial for the provision of financial services for a term of three years from 7 June 2025 to 6 June 2028. Pursuant to the New Financial Services Framework Agreement, the annual cap in respect of the maximum daily balance of deposit (including accrued interests) placed by the Group with SPIC Financial increased from RMB9 billion to RMB12 billion during the effective term of the new agreement. The increase in the annual cap was intended to accommodate the new project companies arising from expected consolidation under the Asset Pre-Restructuring, the anticipated completion of the acquisition of SPIC Hydropower under the Asset Restructuring, and to provide a buffer for the potential issuance of financial instruments to support the Group’s organic growth and future acquisitions. For details, please refer to the circular of the Company dated 21 May 2025.

For the period between 1 January 2025 and 31 December 2025, the maximum daily balance of deposit (including accrued interests) placed by the Group with SPIC Financial was approximately RMB11.97 billion (31 December 2024: RMB8.99 billion), which did not exceed the annual cap.

Pursuant to the aforementioned financial services framework agreements, SPIC Financial provides the Group with an internal treasury management platform, a cross-border fund allocation platform and other financial services through its own financial resources, including the business information system and cross-border fund allocation channels. These platforms enable real-time monitoring of account balances, as well as income and expenditure, thereby safeguarding against funding risks. At the same time, they facilitate flexible and efficient fund allocation across borders, which gives rise to more flexible capital flow at home and abroad, broadens financing channels for domestic subsidiaries and reduces uncertainties in inbound and outbound capital flows due to changes in foreign exchange regulatory policies.

During the year under review, the Group recorded a net increase in cash and cash equivalents of RMB303,553,000 (2024: net increase of RMB334,817,000). For the year ended 31 December 2025:

net cash generated from operating activities amounted to RMB18,518,055,000 (2024: RMB10,621,363,000). The increase was primarily due to the improved working capital management during the year.

net cash used in investing activities amounted to RMB22,683,626,000 (2024: RMB35,172,389,000). The decrease was primarily due to a one-off payment made in 2024 to settle the remaining consideration for the acquisition of certain clean energy companies in October 2023, as well as a year-on-year reduction in payments for property, plant and equipment, and right-of-use assets, and prepayments for construction of power plants.

net cash generated from financing activities amounted to RMB4,469,124,000 (2024: RMB24,885,843,000). The decrease was primarily due to higher year-on-year repayments of bank borrowings and borrowings from related parties.

The financial resources of the Group were mainly derived from cash inflow generated from operating activities, debt instruments, borrowings from banks and related parties, and project financing.

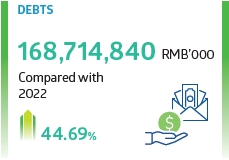

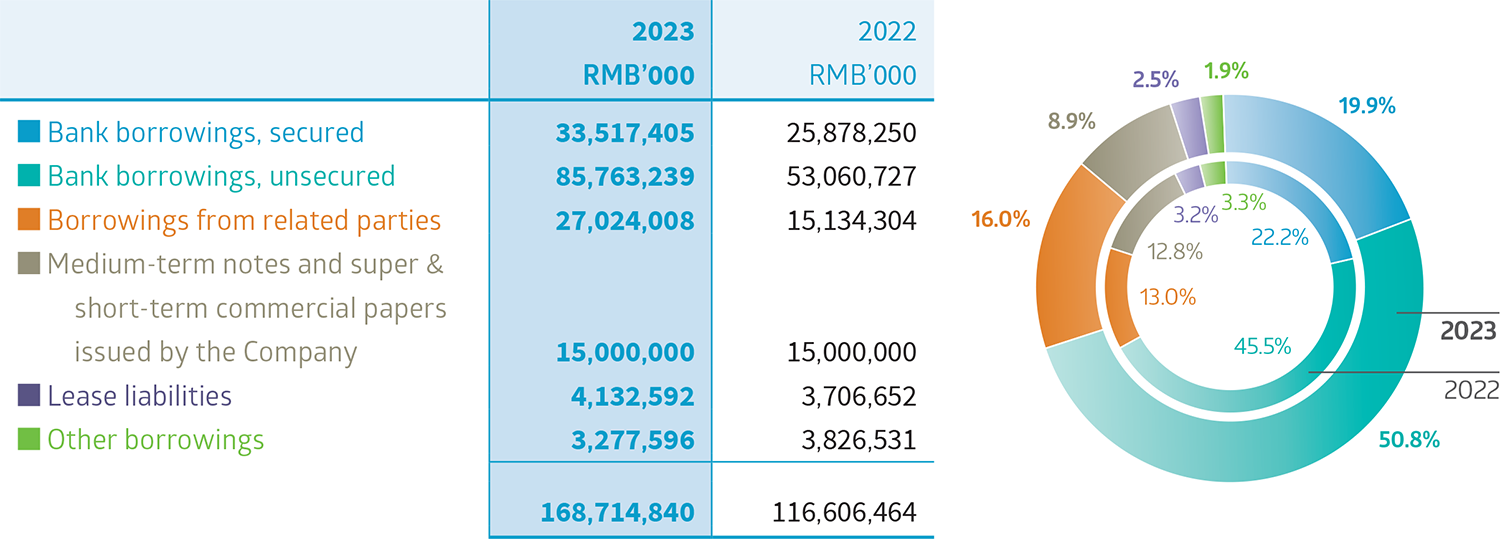

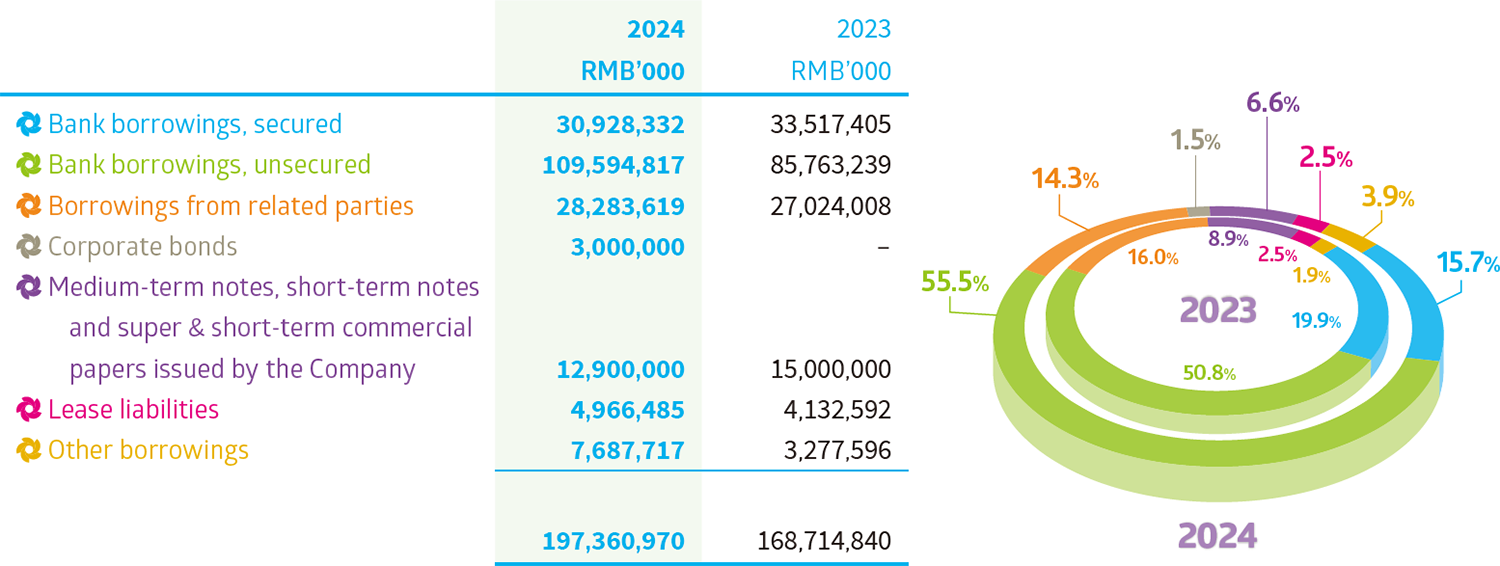

As at 31 December 2025, total debts of the Group amounted to RMB210,329,744,000 (31 December 2024: RMB197,360,970,000). Over 99% of the Group’s total debts are denominated in RMB.

As at 31 December 2025, the Group’s gearing ratio, calculated as net debt (being total debts less cash and cash equivalents) divided by total capital (being total equity plus net debt), was approximately 63% (31 December 2024: approximately 64%). The Group’s gearing ratio remained stable.

As at 31 December 2025, the amount of borrowings from SPIC Financial was approximately RMB12.45 billion (31 December 2024: approximately RMB11.03 billion).

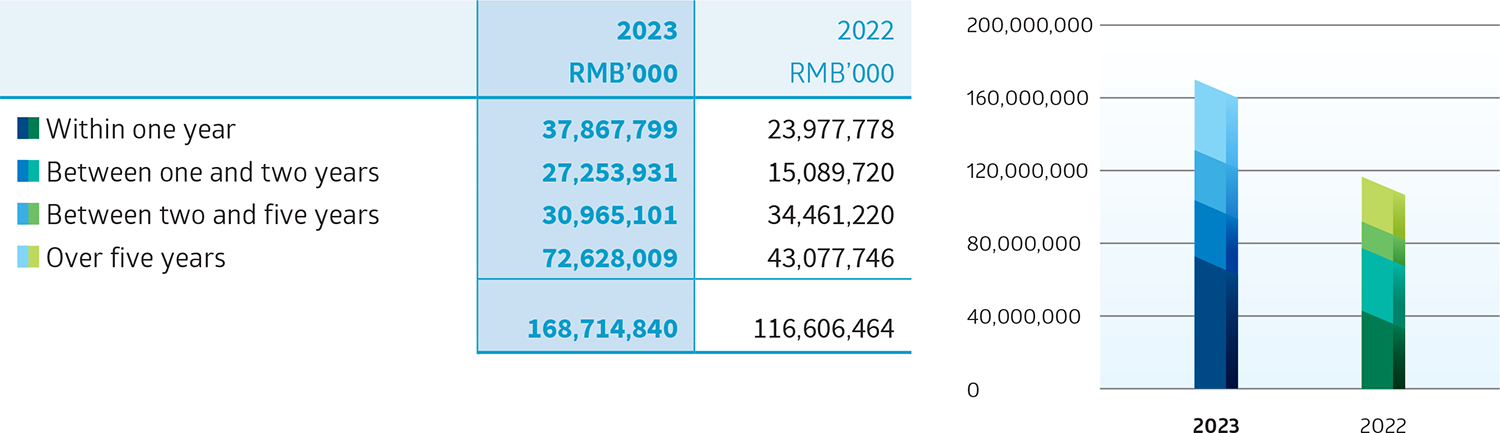

The details of the Group’s debt as at 31 December 2025 and 2024 are set out as follows:

The above debts are repayable as follows:

Among the above debts, approximately RMB75,358,927,000 (31 December 2024: approximately RMB63,916,901,000) are subject to fixed interest rates, and the remaining debts denominated in RMB are subject to adjustment based on the relevant rules of the People’s Bank of China and bearing interest rates ranged from 1.00% to 5.63% (2024: ranged from 1.00% to 4.95%) per annum.

When there is any indication of asset impairment, the Group will conduct an impairment test on the assets to assess whether an impairment has occurred.

In 2025, the Group recognized an impairment of property, plant and equipment totaling RMB47,291,000 (2024: RMB265,262,000). The impairment was primarily due to a photovoltaic power project, where declining tariffs under market-based renewable energy policies result in lower revenue than initial investment projections, leading to an impairment of the related assets.

The Group also recognized an impairment provision for accounts receivable, other receivables and amounts due from related parties (2024: accounts receivable and other receivables) amounting to RMB63,967,000 (2024: RMB228,494,000). The impairment was primarily made on certain long-outstanding prepayments for raw materials and other receivables in relation to subsidies for facility upgrades, which were not expected to be recovered as of the year-end date.

On 25 September 2023, the Company received approval from the National Association of Financial Market Institutional Investors (“NAFMII”, 中國銀行間市場交易商協會) to issue debt financing instruments (“DFI”), with an effective registration period of two years from the approval date. During the effective registration period, the Company is permitted to issue multi-type of DFIs, including but not limited to super & short-term commercial papers, short-term commercial papers, medium-term notes, perpetual notes, asset-backed notes and green debt financing instruments in one or multiple tranches.

During the effective registration period referred to above for the issuance of DFIs, the Company has issued the following instruments during the year:

Save for the proceeds received from the blue bond mentioned above, which have been fully applied towards the construction and operation of a 450MW offshore wind power project of the Company in Shandong Province, as well as to replenish the project’s working capital and repay its interest-bearing debts, all other proceeds from the issuance of DFIs have been fully applied to the repayment of existing borrowings.

On 20 January 2026, the Company obtained another approval from the NAFMII to issue DFI, which is valid for another two-year registration period.

Wu Ling Power has obtained a “Notification on Acceptance of Registration” from the NAFMII, confirming the acceptance of its application for issuance of asset guaranteed debt financing instrument (the “Sci-Tech Note”, 資產擔保債務融資工具(科創票據)) in the PRC by tranches in an aggregate amount of RMB1 billion with an effective registration period of two years from August 2024. On 26 February 2025, Wu Ling Power issued its 2025-first-tranche of the Sci-Tech Note in a principal amount of RMB400 million, at the interest rate of 1.90% per annum with a maturity period of 240 days, to repay its maturing debt.

The Company adopted the Share Incentive Scheme upon the approval by its shareholders at an extraordinary general meeting held on 15 June 2022. Under the Share Incentive Scheme, the Company granted a total of 103,180,000 share options in two tranches in July 2022. All the aforesaid grantees were employees of the Company or its controlled subsidiaries. As at 1 January 2025, there were 58,665,200 shares options granted but not yet lapsed or canceled. There were 11,865,700 share options lapsed during the year under review. Consequently, the Company had 46,799,500 share options outstanding under the Share Incentive Scheme as at 31 December 2025. Taking into account the leaving of grantees and based on the revised estimates of the number of share options that will lapse in the future, the Company recognized share-based payment expenses of RMB2,182,000 (2024: RMB19,283,000) during the year under review.

In 2025, the total capital expenditure of the Group was RMB18,194,290,000 (2024: RMB28,212,560,000). Among them, the capital expenditure for clean energy segments (hydropower, wind power, photovoltaic power and energy storage) was RMB16,163,922,000 (2024: RMB24,583,792,000), which was mainly applied for the engineering construction of new power plants and power stations, and the asset purchases related to the energy storage business; whereas the capital expenditure for thermal power segment was RMB1,103,708,000 (2024: RMB2,872,444,000), which was mainly applied for the technical upgrade for the existing power generating units. These expenditures were mainly funded by project financing, debt instruments, funds generated from business operations and borrowings from related parties.

As at 31 December 2025, certain bank borrowings, borrowings from related parties and other borrowings totaling RMB969,786,000 (31 December 2024: RMB1,546,617,000) were secured by certain property, plant and equipment with a net book value of RMB345,380,000 (31 December 2024: RMB632,581,000). In addition, certain bank borrowings, other borrowings and lease liabilities totaling RMB32,205,759,000 (31 December 2024: RMB31,911,780,000) were secured by the rights on certain accounts receivable amounted to RMB11,732,758,000 (31 December 2024: RMB9,576,998,000). Certain bank borrowings totaling RMB424,677,000 (31 December 2024: Nil) were secured by certain other intangible assets with a net book value of RMB961,080,000 (31 December 2024: Nil).

As at 31 December 2025, the Group had no material contingent liabilities.

In February 2025, the NDRC and the NEA jointly issued Circular No. 136. Circular No. 136 specifies that, in principle, all the on-grid electricity for new energy projects shall enter the electricity spot market and that on-grid tariff shall be derived through market transactions. Circular No. 136 takes 1 June 2025 as the turning point to divide existing and newly added projects, and establishes the “mechanism-based tariff” as the threshold warranty, so as to achieve a seamless integration for the entry of the existing new energy projects into the market at this stage. For the existing new energy projects that commenced production before 1 June 2025, the mechanism-based tariff shall be implemented at a certain percentage of the electricity generated and based on the benchmark tariff for coal-fired power, and the price difference shall be settled. For newly added projects that commenced production after 1 June 2025, the proportion of electricity to be included in the mechanism will be dynamically adjusted, and the mechanism-based tariff will be derived according to the bidding process of newly commissioned projects.

In addition to allowing the entry of new energy into the market under Circular No. 136, the NDRC and the NEA jointly issued the “Circular on Comprehensively Accelerating the Development of the Electricity Spot Market” (“Circular No. 394”) in April 2025, which requires that the full coverage of the electricity spot market be basically realized on a national basis by the end of 2025, and that continuous settlement be carried out comprehensively, giving full play to the key role of the spot market in identifying prices and regulating the supply and demand. The significance of Circular No. 394 lies in, among others, once again recognizing the distinctive role of the electricity spot market in optimizing resource allocation, procuring safe power supply, and promoting the renewable energy consumption. It once again clarifies the timetable for the establishment of the spot market for electricity trading, and urges the speedy development of spot markets in certain provinces.

In April and May 2025, the NDRC and the NEA jointly issued the “Guiding Opinions on Accelerating the Development of Virtual Power Plants” and the “Circular on Organizing and Carrying Out the First Batch of Pilot Work for the Construction of New-type Power Systems”, proposing to accelerate the comprehensive participation of virtual power plants in the medium-to-long-term power markets and spot market transactions as a new type of resource aggregation business entity and clarify the corresponding principles for calculating electricity volumes and electricity charges. The participation of virtual power plant in power sale and purchase business in the medium-to-long-term power market as well as spot market can help to enhance the price formation mechanism in the medium-to-long-term power market, and appropriately expand the price limit range in the spot market.

In October 2025, the NEA issued the “Guiding Opinions on Promoting the Integrated Development of Coal and New Energy” (the “Guiding Opinions”) to promote the development of a new paradigm for the coordinated development of the traditional and new energy, which plays an important role for strengthening the foundation of steady energy supply and promoting green and low-carbon energy transformation. The Guiding Opinions proposed accelerating the development of photovoltaic and wind power industries and actively promoting the replacement with clean energy for existing energy use in mining areas. The related policy-driven market demands for the upgrades and construction of power facilities as well as for the green electricity-related markets will become a key direction for the business expansion of the Group.

The Group will strengthen the review of the market conditions and the analysis of economic activities, closely monitor key indicators such as electricity volume and tariff, and optimize the priority and structure of power generation to strive for opportunities to generate electricity and promote power sales. In addition, the Group will also continue to optimize various types of power sources to flexibly respond to the changing market environment.

| Address | Suite 6301, 63/F, Central Plaza, 18 Harbour Road, Wanchai, Hong Kong |

| Phone | (852) 2802-3861 |

| Fax | (852) 2802-3922 |

| ir@chinapower.hk |